Income Taxes reflect this share, serving as a reminder that not all earnings translate to net profit. When this figure grows, businesses know they’re onto something; when it dwindles, it’s a clarion call to introspection. Our website services, content, and products are for informational purposes only. Losses from a lawsuit are generally recorded before the actual payment is made. This is because the loss from a lawsuit is normally recorded based on an estimate when the loss is considered probable to happen.

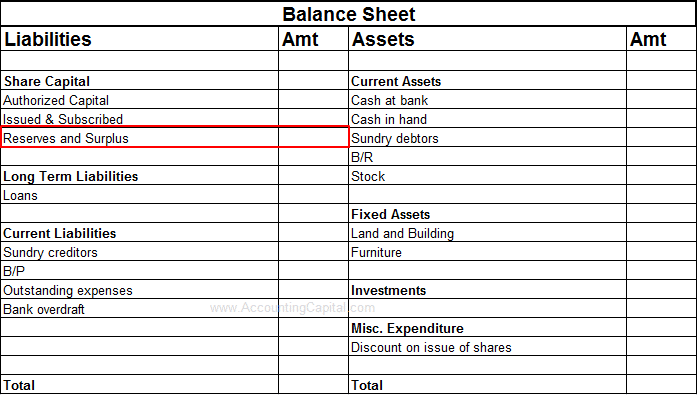

What are the three core documents that measure a company’s performance?

Dividends constitute another aspect of shareholder returns that can take a hit. Companies that regularly pay dividends may opt to reduce or eliminate them to preserve cash amidst tough financial conditions. This may disappoint income-seeking investors who rely on regular dividend payouts. This is recorded by making a debit entry to the account titled “Bad Debts Expense” and a corresponding credit entry to the “Allowance for Doubtful Accounts” account. In financial accounting, the treatment and recording of losses vary depending on the nature of the loss.

Types of P&L Statements

If you prefer to opt out, you can alternatively choose to refuse consent. Please note that some information might still be retained by your browser as it’s required for the site to function. Skylar Clarine is a fact-checker and expert in personal finance with a range of experience including veterinary technology and film studies. A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise.

Gains and Losses vs. Revenue and Expenses: What’s the Difference?

Clubbing them with regular income or expenses can paint a distorted image of business health. However, Gross Profit doesn’t account for other expenses that companies incur. Yet, it’s essential as it offers an initial glimpse into the efficiency of the production and pricing processes.

What is the purpose of a Profit and Loss Statement?

Other businesses, such partnerships, are flow-through entities, which require the owners to report and pay taxes on their share of the business’ income. Capital losses sustained during the year must be first used to offset other capital gains. If capital losses exceed any capital gains made during the year, only a portion of it may be used to offset other taxable income.

In economics, when an agent is risk neutral, the objective function is simply expressed as the expected value of a monetary quantity, such as profit, income, or end-of-period wealth. For risk-averse or risk-loving agents, loss is measured as the negative of a utility function, and the objective function to be optimized is the expected value of utility. “Loss”, sometimes referred to as “Loss.jpg”,[1] is a strip published on June 2, 2008, by Tim Buckley for his gaming-related webcomic Ctrl+Alt+Del.

- Still different estimators would be optimal under other, less common circumstances.

- Losses adversely affect the stock prices, and the shrinking of market capitalization might even instigate a vicious cycle of devaluation.

- Insurance serves as a strategic tool for businesses to manage financial losses by transferring risk to a third party.

- All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

- There’s a fundamental accounting principle, known as the matching principle, which requires that losses be matched with revenues in the period they are incurred.

It is also used to refer to several periods of net losses caused by expenses exceeding revenues. A profit and loss statement, also called an income statement or P&L statement, is a financial document that summarized the revenues, costs, and expenses incurred by a company during a specified period. They decrease the assets, increase the liabilities, or reduce the overall equity of a company. There’s a fundamental accounting principle, known as the matching principle, which requires that losses be matched with revenues in the period they are incurred.

The reason behind this is that any changes in revenues, operating costs, research and development (R&D) spending, and net earnings over time are more meaningful than the numbers themselves. For example, a company’s revenues may grow on a steady basis, but its expenses might grow at a much faster rate. A profit and loss statement, also called an income statement or P&L statement, is a financial document that summarizes the revenues, costs, and expenses incurred by a company during a specified period. The ability to carry losses not only forward to offset future profits, but also backward to recoup previously paid taxes, allows businesses to maximize their tax efficiency. By using these tools, companies can align their tax strategies with their financial goals, creating a more effective plan for growth and profitability.

Explore strategies for handling financial losses in business, including accounting practices, insurance roles, and reporting obligations for a robust fiscal approach. Yet another example would be of a company that sells frozen foods and needs to pay for who files schedule c: profit or loss from refrigerated storage facilities, utility costs, taxes, employee expenses, and insurance. If sales are slow, the company will need to hold onto its inventory for a longer time, incurring additional carrying costs which could contribute to a net loss.

This accounting treatment can provide a financial cushion, as it may reduce the tax burden in profitable years. Companies must adhere to the tax laws governing the carryover of losses, which vary by jurisdiction. Financial losses are an inevitable aspect of running a business, and their management is crucial for long-term sustainability. These losses can stem from various sources such as operational failures, market downturns, or unforeseen events, impacting the financial health of a company.